All The Fintech - Neobanks - 4.12.19

All The Fintech - Neobanks - 4.12.19

The So What

2019 looks to be shaping up to be a very interesting year for fintech - particularly in regards to “neobanks” which got me thinking, what the heck is a neobank anyways? Well thankfully there’s already a wikipedia page with an attempt at a definition: “a type of direct bank that is 100% digital and reaches customers on mobile apps and personal computer platforms only.”

In 2018 - 2019, we’ve seen some big ‘unicorn’ valuations for a variety of neobanks in the US + abroad including Chime, Revolut, N26, and most recently Monzo (“rumored”). So what’s the big deal? I thought a quick comparison between Chime vs Chase could be interesting…

Chime

Founded in 2013 by Chris Britt and Ryan King, launched in 2014. On Sept 2017, announced their $18MM series B with 500,000 bank accounts opened and expecting to reach $1B in transaction volume by the end of the year.

Less than a year later on June 2018, Chime announced their $70MM series Cwith a $500MM valuation with over 1MM+ opened accounts, adding >100k new bank accounts / month, $4.5B in transaction volume, and saving accounts holding about $150 million (implying an average of $150 / account) - all with just an 80 person headcount.

Less than a year later on March 2019, Chime announced their $200MM series D with a $1.5B valuation with over 3MM opened accounts, adding 200k new accounts / month - all with just a 120 person headcount.

CAC and LTV strategy aside, Chime has been able to quickly acquire users with a highly effective, lean, technology enabled team and that rate continues to accelerate. The longer term bet is that as their users continue to engage with Chime and move from underbanked, they’ll continue to transact using the debit card on larger transactions (interchange revenue), deposits under management will continue to increase (deposit revenue), and Chime will continue to offer other financial products (fee based revenue).

Chase

One of my other favorite things to do (sorta joking but not really…) is reading through investor day presentations by large FIs to get a sense of what their strategies are. Banks are unique in that because they’re so large, their development + product strategies are typically set years in advance so what’s generally stated to Wall Street gives a glimpse into the next few years’ priorities.

Chase’s investor day presentation had some really fun stats, including…

Scale

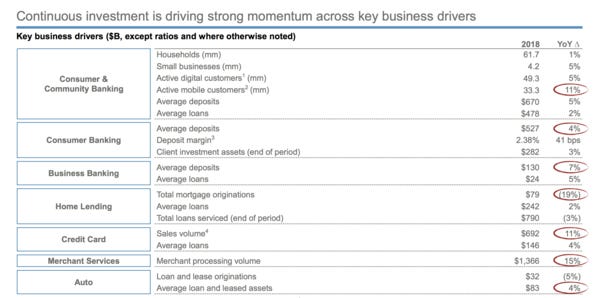

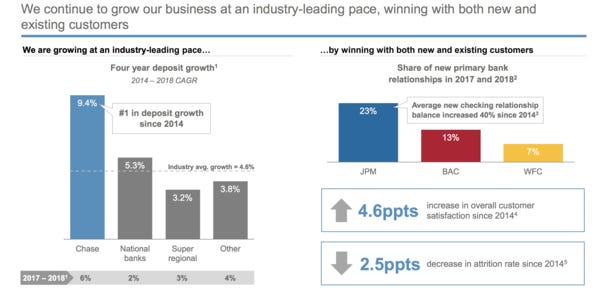

Chase banks 62mm households and 4mm SMBs, which represents ~50% of US households. Out of their total consumer base, 22mm are active on mobile (active being defined as users of all mobile platforms who have logged in within the past 90 days, which is also a very interesting way to define that KPI…). This gives Chase the largest active mobile customer base amongst US banks as well as the fastest-growing mobile banking customer base. Chase has also been #1 in new primary bank relationships in 2018 with 9% of the retail deposit market share, and has issued over 99MM debit and credit accounts.

In regards to digital channels, Chase has opened 1.5MM deposit accounts since Feb 2018 to Feb 2019 and the average deposit across all consumer accounts is $527.

TLDR

While Chase’s Community and Corporate Banking division does have a much larger and more sophisticated business with credit cards, home lending, etc - it’s still really quite impressive to see what growth a tech-first neobank such as Chime can accomplish with 120 people vs Chase at 140,000 people. There are obviously nuances and lots of questions still to be answered about long term viability and whether the growth rate is sustainable, but increasingly so it does feel as though large banks are realizing that all of these upstarts could actually affect the bottom line and the need to focus on product quality is all the more important - and makes these unicorn valuations seem a little less out there :).

Chase Key Business Drivers

Deposit growth rate at 6% CAGR

Focus on mobile engagement