All The Fintech - 10.10.19 - The start of the midgame for fintech companies

All The Fintech - 10.10.19 - The start of the midgame for fintech companies

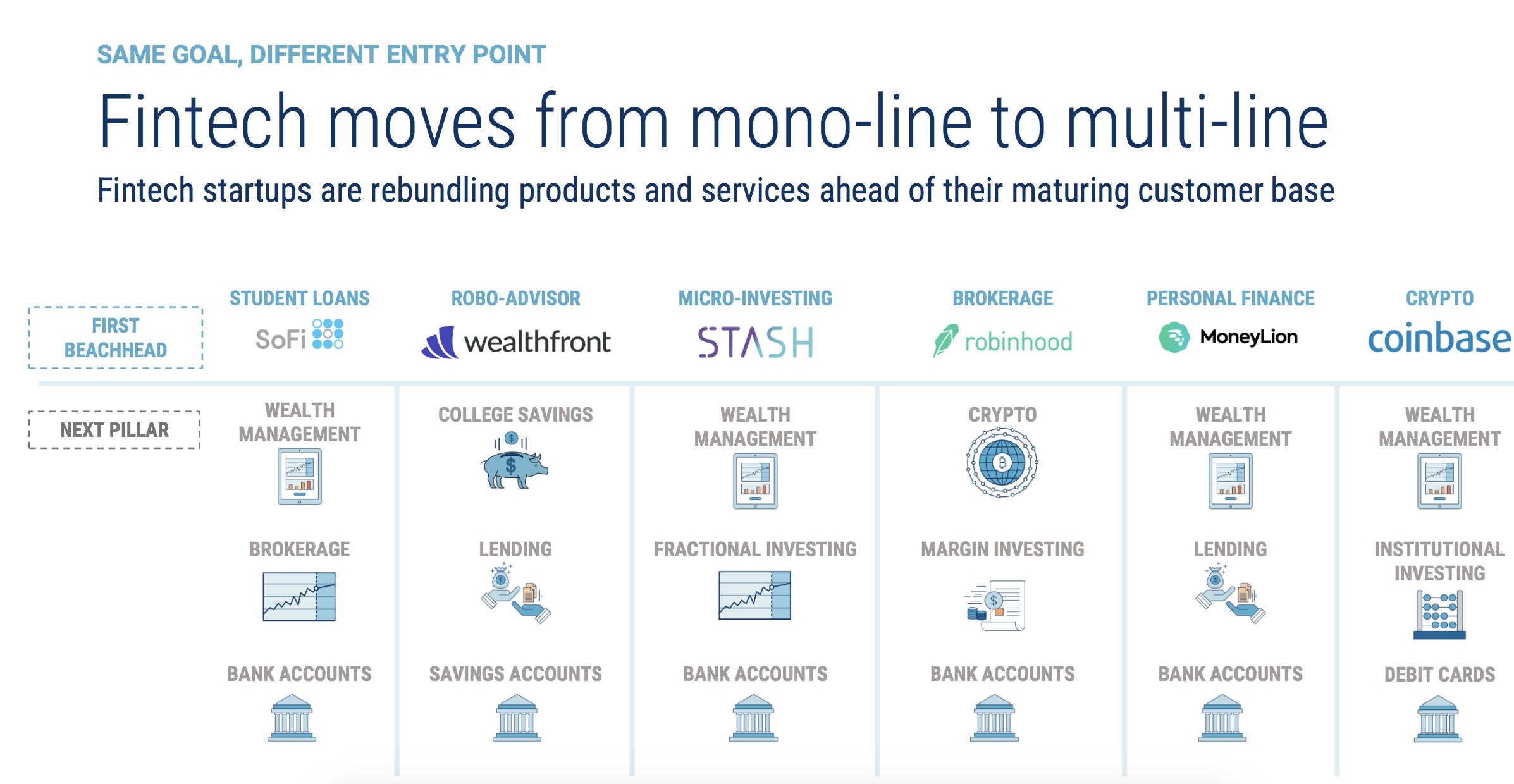

This year has been really interesting as I believe we’re starting to see the mid-game strategy of several fintech companies making their moves from mono-line product offerings to try and become end to end platforms with a variety of new product offerings. The typical high growth playbook in fintech has been identifying a differentiated product wedge, acquiring as much scale (aka user whether they be business or consumers) as quickly + efficiently as possible, and investing into newer product offerings to cross-sell. The tech multiple assumption built into these companies is partially built on the belief that they’ll be able to retain the users they’ve acquired with the initial product and convince those users to run a majority of their financial lives on the platform.

In just the past week, we’ve seen Brex launch their B2B cash account, Robinhood re-announce their high yield checking + debit product, and Credit Karma launch a high-yield savings account. In the past quarter, Stripe publicly launched their corporate and capital program, Betterment announced their high yield savings (Wealthfront did so already in Feb), and Sofi even forayed into crypto trading. In my opinion, the key difference between a true platform company vs a company with multiple products is the ability to leverage a single view of the customer to offer differentiated and unified product experiences vs silo’ed data views of the customer for each individual product offering. Each product should also contribute meaningful + high signal data back to the platform, thus creating a product feedback loop as well as platform lock-in.

For example in Brex’s case, the cash account allows them to expand their addressable market outside of companies they currently know how to underwrite for revolving credit to any business that needs a bank account - this also unlocks additional revenue streams such as durbin-exempt interchange + other financing options (Brex Capital anyone?), with the end goal of becoming the end to end platform to run a business on top of. For Robinhood, a cash management account encourages users to keep funds in the platform which ideally leads to more trade volume, more premium subscriptions, and that sweet interchange + net interest income revenue. Interestingly enough, the fee landscape in consumer brokerage is also finally shifting with 6 of the largest brokerages announcing in the past two weeks that they’re now offering zero-commision online trades, wiping a combined $20B in market cap.

Time will tell as to which initial product wedge brings in the ideal, lasting customer and which companies can successfully build out a growth platform - in B2B there’s been success in building out platforms with companies like Square (initial wedge: payment processing + merchant underwriting), Shopify (initial wedge: online storefronts), and even Wave which H&R Block picked up this year (accounting). On the consumer side, it’s still early days of the mid-game :).

On the enterprise side, there’s also been a movement of financial institutions trying to move to a platform approach driven by technology rather than a sales team. My favorite early barometer to test for data silos with any financial application is simply going through onboarding for one product (e.g. savings) and then opening another product a few days later (e.g. brokerage) to see how many data points are repeated - more often than not I have to completely re-onboard. “Disruption” of financial services can perhaps be distilled down to - can emerging fintech companies use technology to create a full-service, platform business for their users faster than large incumbents refactoring/rebuilding silo’ed products, users, and data? The honest answer is probably involves some winners and losers (and partnerships) on both sides and I’m excited to see it play out as a consumer!

Related reads:

CB Insights has a fun read on fintech startups and where they got their initial users

Brendan Dickinson distilling his framework on fintech companies -

Recently, I’ve begun to think of fintech within a new framework: financial platforms, financial product manufacturers and financial infrastructure providers. Financial platforms earn a customer’s trust by solving an immediate pain point and leveraging that position to take over more of their financial life. Financial product manufacturers create and distribute new (or traditionally offline) financial products. Financial infrastructure companies build the connective tissue of a modern financial ecosystem.

Some (somewhat accurate) information on the Durbin Amendment -